Smaller cities with lower home prices were once again among the top-performing housing markets this month, a trend that started emerging in January this year, according to the latest report from realtor.com®.“We’re seeing more interest in secondary markets,” says Danielle Hale, realtor.com®’s chief economist. “Homes are a little bit more affordable, and buyers are looking for that affordability.”Midland, Texas, once again toppe

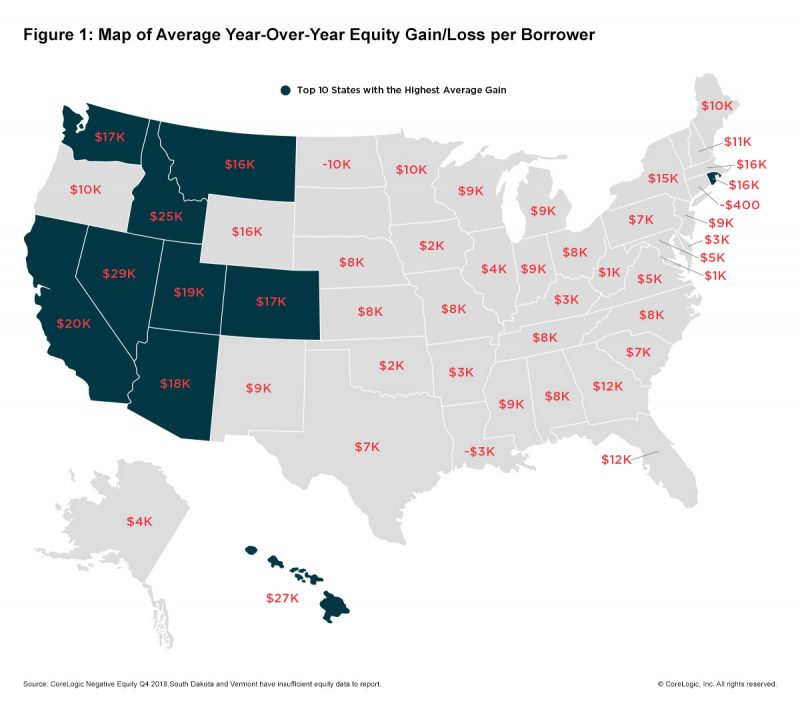

Home equity continued to increase in the fourth quarter of 2018, with more homeowners profiting over rising home prices. U.S. homeowners with a mortgage saw their equity rise by 8.1 percent year over year in the fourth quarter of 2018, according to CoreLogic’s Home Equity Report, released Thursday.The average homeowner has gained $9,700 in home equity between the fourth quarter of 2017 and the fourth quarter of 2018, the report showed. Western

Sales of newly built single-family homes picked up at the end of last year, reaching the highest level since May 2018, a newly released report from the U.S. Commerce Department shows. New-home sales increased 3.7 percent in December to a seasonally adjusted annual rate of 621,000 units (the number of homes that would sell if this pace continued over the next 12 months).“Despite a period of weakness in the fall, new home sales ended the year wit

Vietnamese investors are increasingly gaining on China as a significant source of participants in a foreign investment initiative by the United States that provides green cards for investing in U.S. real estate, The Wall Street Journal reports. The program, the EB-5 Immigrant Investor Program, offers green cards to those who invest in job-creating U.S. businesses or real estate projects. The percentage of EB-5 visas issued to Vietnamese

For average-sized homes, buying a home is usually a better deal than renting, says a new study by LendingTree, an online lending resource, which compared monthly rental and mortgage payments for homes in the 50 largest U.S. metros.“Renting can be the best option if a person is not planning on staying in one area for a very long time or does not have enough cash for a down payment,” LendingTree notes in its study. “But buying a home can be a

The majority of Americans—79 percent recently surveyed—still believe that owning a home is a vital component of achieving the American dream, according to a Bankrate.com survey of more than 2,000 consumers. Americans placed achieving homeownership ahead of retirement (68 percent), having a successful career (63 percent), and owning an automobile (58 percent), according to the survey.While the majority of respondents rated ownership high, they

Minneapolis may offer the most possibilities for low-income households to become homeowners. The city has the nation’s highest homeownership rate among households in the bottom 25 percent of income at 57.7 percent, according to a new analysis from Redfin of the 50 largest metros. Pittsburgh and St. Louis followed on the list, also having homes that tend to sell for less than the national median of $285,000.“Homeownership allows people to shar

Buyers financing their home purchase can save hundreds of dollars in their first year of owning just by shopping around for a mortgage, according to new study from NerdWallet, a personal finance website.Home shoppers who compare interest rates between five different lenders can pocket $430 in savings in their first year alone, according to NerdWallet’s analysis using a 30-year fixed-rate, $260,000 mortgage.“That savings would accumulate and c

More Americans are paying their mortgages on time than at any point in nearly two decades, according to the Mortgage Bankers Association.Delinquency rates are a key economic measure, closely watched by economists. The last time a large number of homeowners stopped making mortgage payments on time, from 2007 to 2008, it impacted the entire economy.Borrowers who have conventional mortgages are the most likely to pay on time, while borrowers with lo

In 2017, small-town America gained residents for the first time in decades, according to U.S. Census Bureau data.“Moving to a small town lets people afford a quality of life that is really appealing and lets them feel like a part of a community … in a way that so many young people are looking for today,” says Winona Dimeo-Ediger, editor of Livability.com.For the third year, realtor.com® identified America’s best small towns by analyzing

This website includes images sourced from third party websites including Adobe, Getty Images, and as otherwise noted.