Fewer investors are flipping homes, but those still active in the market are earning higher profits. Typical investment returns rose to the highest level since late 2018 for housing flips, according to ATTOM Data Solutions’ latest 2020 U.S. Home Flipping Report.The gross profit on the typical home flip nationwide—which is reflected as the difference between the median sales price and the median paid by investors—rose to $67,902 in the secon

Record low mortgage rates are drawing a new wave of first-time home buyers to the market, Freddie Mac reports. “In August, activity among first-time home buyers rose 19% from July to the highest monthly level ever for Freddie Mac,” says the mortgage giant’s Chief Economist Sam Khater, adding that the rebound “has come at a critical time for the economy.”Since the beginning of the year, mortgage rates have dropped more than 80 basis poin

Home shoppers may have an even tougher time finding a home to purchase in the weeks and months to come, as home prices continue to climb and even fewer new listings arrive on the market.Home price growth has reached a two-year high, while natural disasters brought the number of homes for sale even lower, according to realtor.com®’s Weekly Housing Report, reflecting the week ending Sept. 12. Still-strong buyer demand but lack of supply prompted

The Federal Reserve voted Wednesday to leave its benchmark lending rate unchanged and near zero. It will likely stay in place for more than a year to help the economy recover from the COVID-19 pandemic.The Fed’s benchmark rate is what banks charge one another for short-term borrowing. It is not the rate consumers pay, and it doesn’t often directly influence mortgage rates, although it does often have an impact.The committee on Wednesday also

The 30-year fixed-rate mortgage continues to hit new all-time lows practically on a monthly basis. That has dramatically increased the pool of homeowners who could benefit from refinancing and lowering their monthly mortgage payment. In fact, 75% of homeowners—or 19.3 million—could benefit from refinancing, according to data from Black Knight, a software and analytics firm for the mortgage and lending industry. That's the largest number of po

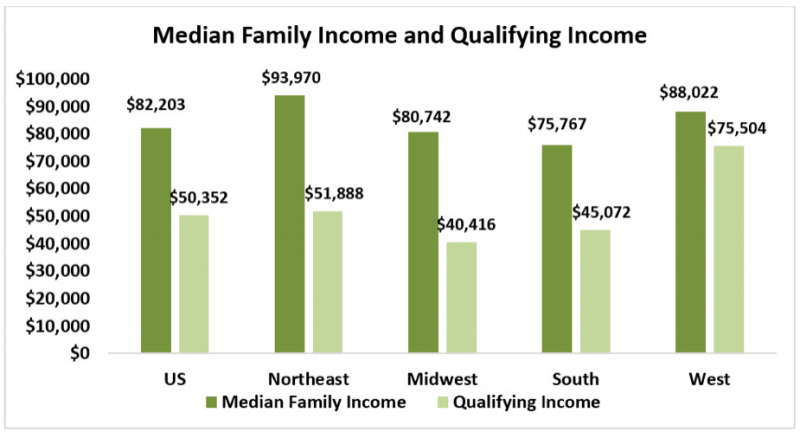

From June to July, median sales price rose by 8.5%, more than double the 4.1% increase seen in family income levels, the National Association of REALTORS® reports. But mortgage rates that have fallen to all-time lows are helping to offset some of the rising costs.As of July, all of the national and regional data in NAR’s affordability index was above 100, which means a family with a median income had more than the income required to afford a m

Waterfront homes have been growing in demand since the COVID-19 pandemic began in spring. Sales of lakefront homes have increased more than 40% year over year, Glenn S. Phillips, CEO and lead economic analyst at LakeHomes.com, told realtor.com®.“People saw their friends and family go to the lake and realized that if you are social distancing and home schooling, the lake is a far better place than most primary residences,” Phillips told realt

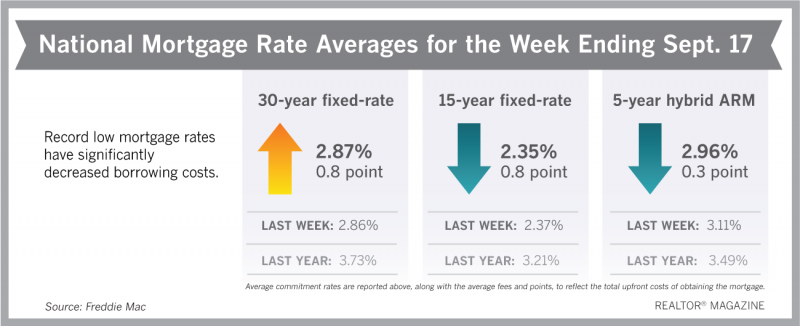

Just as some housing experts were predicting rates couldn’t get lower, they did. The 30-year fixed-rate mortgage reached a new all-time low, averaging 2.86% this week, according to Freddie Mac. “Mortgage rates have hit another record low due to a late-summer slowdown in the economic recovery,” says Sam Khater, Freddie Mac’s chief economist. “These low rates have ignited robust purchase demand activity, which has been growing at double-d

The home shopping spree continues. Typically, the end of August sees a slowdown in the housing market, but this year, real estate has shown no signs of letting up.Mortgage applications to purchase a home increased 3% last week compared to the previous week. But it’s the year-over-year jump of 40% that has surprised economists. Year-over-year comparisons are usually in the single digits.“There continues to be resiliency in the purchase market,

The most affordable housing markets in the U.S. tend to be located in the South and Midwest, according to a new analysis from RefiGuide.org, a home refinance resource. For example, Youngstown, Ohio, topped the list as the most affordable place in the country, where the median household income in one year is more than the typical purchase price of a home.On the other end of the spectrum, however, California tends to have the least affordable housi

This website includes images sourced from third party websites including Adobe, Getty Images, and as otherwise noted.